Cause, Network Dynamics, And Modelling Approaches for Financial Stability

This research explores how financial shocks propagate through interbank networks, the mechanisms underlying systemic risk, and the modeling approaches used to assess and enhance the stability of Indonesia’s banking system.

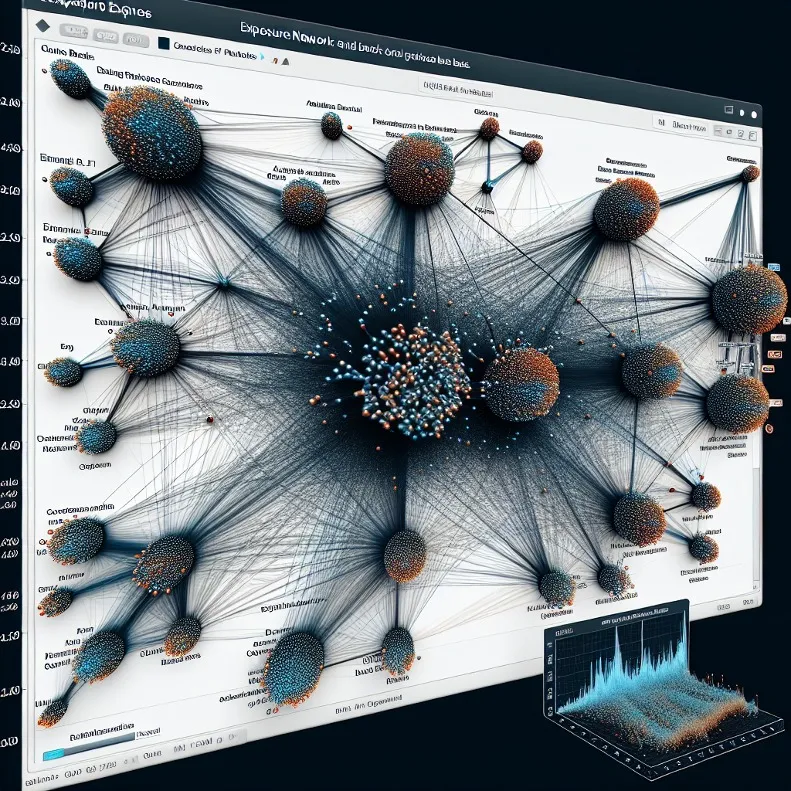

Interbank Exposure Network Visualization

Financial Contagion

Systemic Risk

Interbank Interconnectedness

Credit Risk

Capital Shortfall

Financial Network Analysis

Financial System Stability

Indonesian Banking

Legend: Key Variables

Financial Contagion:The process by which financial shocks or distress spread from one bank to others within the network.

Systemic Risk:The risk that the failure of one or more banks could trigger instability or collapse of the entire financial system.

Interbank Interconnectedness:The degree to which banks are linked to each other through financial exposures, such as loans or credit lines.

Credit Risk:The risk of loss arising from a counterparty’s failure to meet its financial obligations.

Capital Shortfall:A situation where a bank’s capital is insufficient to absorb losses, potentially leading to insolvency.

Financial Network Analysis:The use of network theory and tools (such as Gephi) to study the structure and dynamics of financial relationships among banks.

Financial System Stability:The resilience of the banking sector to shocks and its ability to function effectively without widespread failures.

Indonesian Banking:The context of the analysis, focusing on banks operating within Indonesia’s financial system.